Scammers are taking advantage of fears surrounding the Coronavirus.

Avoid Coronavirus Scams

Here are some tips to help you keep the scammers at bay:

- Hang up on robocalls. Don’t press any numbers. Scammers are using illegal robocalls to pitch everything from scam Coronavirus treatments to work-at-home schemes. The recording might say that pressing a number will let you speak to a live operator or remove you from their call list, but it might lead to more robocalls, instead.

- Ignore online offers for vaccinations and home test kits. There currently are no vaccines, pills, potions, lotions, lozenges or other prescription or over-the-counter products available to treat or cure Coronavirus disease 2019 (COVID-19) — online or in stores. At this time, there also are no FDA-authorized home test kits for the Coronavirus. Visit the FDA to learn more.

- Fact-check information. Scammers, and sometimes well-meaning people, share information that hasn’t been verified. Before you pass on any messages, contact trusted sources. Visit What the U.S. Government is Doing for links to federal, state and local government agencies.

- Know who you’re buying from. Online sellers may claim to have in-demand products, like cleaning, household, and health and medical supplies when, in fact, they don’t.

- Don’t respond to texts and emails about checks from the government. The details are still being worked out. Anyone who tells you they can get you the money now is a scammer.

- Don’t click on links from sources you don’t know. They could download viruses onto your computer or device.

- Watch for emails claiming to be from the Centers for Disease Control and Prevention (CDC) or experts saying they have information about the virus. For the most up-to-date information about the Coronavirus, visit the Centers for Disease Control and Prevention (CDC) and the World Health Organization (WHO).

- Do your homework when it comes to donations, whether through charities or crowdfunding sites. Don’t let anyone rush you into making a donation. If someone wants donations in cash, by gift card, or by wiring money, don’t do it.

Economic Slowdown: What the Experts Are Saying

More and more economists are predicting a recession is imminent as the result of the pullback in the economy caused by COVID-19. According to the National Bureau of Economic Research:

Bill McBride, the founder of Calculated Risk, believes we are already in a recession:

How deep will it go?

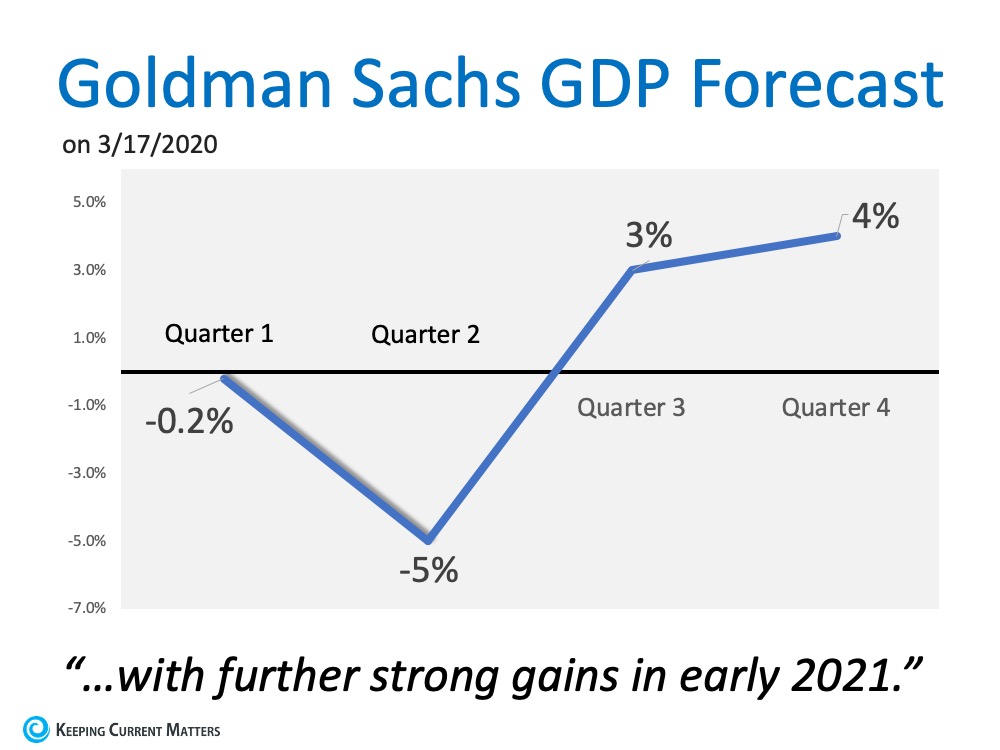

No one knows for sure. It depends on how long it takes to beat this virus. Goldman Sachs anticipates we will see a difficult first half of the year, but the economy will recover in the second half (see below): Goldman also projects we’ll have “further strong gains in early 2021.”

Goldman also projects we’ll have “further strong gains in early 2021.”

This aligns with the projection from Wells Fargo Investment Institute:

Again, no one knows for sure how long the pandemic will last. The hope is that it will resolve sometime over the next several months. Most agree that when it does, the economy will regain its strength quickly.

*Quarter 1 data from Goldman Sachs was updated from 0% to -0.2% on 3/17/20 after the initial release.

This virus is not only impacting the physical health of Americans, but also the financial health of the nation. The sooner we beat it, the sooner our lives will return to normal. Call me today if you need anything during this difficult time. Take Control and Work with Stovall Team. Whether you’re considering selling your home or feeling the challenges as a buyer, you can take advantage of current real estate trends by taking control and working with us at Stovall Team. This year has been one of twists and turns for the real estate market. As with every real estate year, the market can shift in an instant. Call today 714.343.9294 to see if the time is right.