As more people continue to identify their changing needs this year, some are turning to the upscale housing sector for more space or finer features. In their most recent Luxury Market Report, the Institute for Luxury Home Marketing (ILHM) shares:

“In a snapshot of 2020, despite the devasting effects of the coronavirus pandemic, the luxury real estate market has seen one of its strongest years since 2008. In comparison to experts’ predictions in early 2020, it is remarkable how significant demands for property type, location, and amenity preferences have changed amid the pandemic.”

With more opportunities to work from home and a growing interest in having extra space for things like virtual school, working out, and cooking more meals, the desire to own a home that can meet these needs continues to increase. Additionally, record-low mortgage rates are creating opportunities for homebuyers to stretch their legs into higher price points or even expand their real estate portfolios. The ILHM report continues to say:

“Experts believe that the demand for exclusive residential properties outside the metropolitan areas will continue well into 2021; even with the introduction of vaccines, the pandemic is far from over.

For those who have moved to the suburbs and beyond, moving back to the city full time is unlikely while the work from home trend remains. Many of these affluent homeowners are now making their secondary properties their primary residences for the foreseeable future.”

If you’re interested in buying a home this year, it appears that some higher-priced markets may have more homes to choose from than those at lower price points. Javier Vivas, Director of Economic Research at realtor.com, notes:

“Interestingly, markets, where new supply is improving the fastest, tend to be higher priced than those that have yet to see improvement, suggesting sellers are more active in the more expensive markets.”

Bottom Line

If you’re hoping to buy the home of your dreams, this could be the year to achieve that goal. Connect with Stovall Team at 714.343.9294 [email protected] today to explore your possibilities.

Is It Time to Buy a Bigger Home?

In today’s housing market, all eyes are on millennials. Not only are millennials the largest generation, but they’re also currently between 25 and 40 years old. These are often considered prime homebuying years when many people begin to form their own households and invest in real estate. If you’re like many millennials who are spending much more time at home these days, you may have a growing need for more space or upgraded features, making moving more desirable than ever.

For those millennials who already own a home, there’s a great opportunity to move up in 2021. Danielle Hale, Chief Economist at realtor.com, explains:

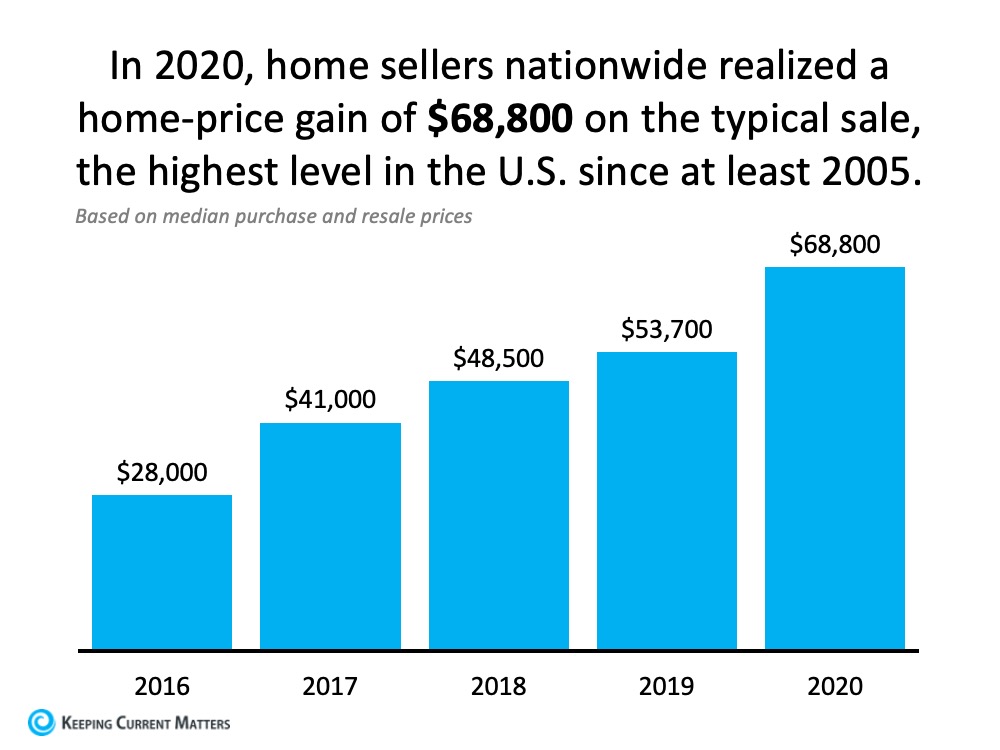

Even if you bought a home sometime in the last few years, you may have more equity than you realize, and that’s a big factor to consider when you’re thinking about moving. According to the Homeowner Equity Insights Report from CoreLogic:

Growing equity can be the driver you’re looking for to fund your next move, especially if what you need in a home is changing right now. As equity builds over time, it can be put toward the down payment on your next home.

In addition to equity gains, today’s housing market affordability is powered by record-low mortgage rates, so moving at a time when you can get more for your money may be more realistic than you think.

Bottom Line

If you’re thinking about moving this year, you’re not alone. Contact Stovall Team at 714.343.9294 to shed light on the equity you have in your current home and the opportunities it can create.