Today’s homebuyers are faced with a strong sellers’ market, which means there are a lot of active buyers competing for a relatively low number of available homes. As a result, it’s essential to understand how to make a confident and competitive offer on your dream home. Here are five tips for success in this critical stage of the homebuying process.

1. Listen to Stovall Team

An article from Freddie Mac gives direction on making an offer on a home. From the start, it emphasizes how trusted professionals can help you stay focused on the most important things, especially at times when this process can get emotional for buyers:

“Remember to let your homebuying team guide you on your journey, not your emotions. Their support and expertise will keep you from compromising on your must-haves and future financial stability.”

Stovall Team’s Micah Stovall is the expert guide you lean on for advice when you’re ready to make an offer.

2. Understand Your Finances

Having a complete understanding of your budget and how much house you can afford is essential. The best way to know this is to get pre-approved for a loan early in the homebuying process. Only 44% of today’s prospective homebuyers are planning to apply for pre-approval, so be sure to take this step so you stand out from the crowd. Doing so make it clear to sellers you’re a serious and qualified buyer, and it can give you a competitive edge in a bidding war.

3. Be Prepared to Move Quickly

According to the latest Realtors Confidence Index from the National Association of Realtors (NAR), the average property sold today receives 3.7 offers and is on the market for just 21 days. These are both results of today’s competitive market, showing how important it is to stay agile and alert in your search. As soon as you find the right home for your needs, be prepared to submit an offer as quickly as possible.

4. Make a Fair Offer

It’s only natural to want the best deal you can get on a home. However, Freddie Mac also warns that submitting an offer that’s too low can lead sellers to doubt how serious you are as a buyer. Don’t make an offer that will be tossed out as soon as it’s received. The expertise your agent brings to this part of the process will help you stay competitive:

“Your agent will work with you to make an informed offer based on the market value of the home, the condition of the home and recent home sale prices in the area.”

5. Stay Flexible in Negotiations

After submitting an offer, the seller may accept it, reject it, or counter it with their own changes. In a competitive market, it’s important to stay nimble throughout the negotiation process. You can strengthen your position with an offer that includes flexible move-in dates, a higher price, or minimal contingencies (conditions you set that the seller must meet for the purchase to be finalized). Freddie Mac explains that there are, however, certain contingencies you don’t want to forego:

“Resist the temptation to waive the inspection contingency, especially in a hot market or if the home is being sold ‘as-is’, which means the seller won’t pay for repairs. Without an inspection contingency, you could be stuck with a contract on a house you can’t afford to fix.”

Bottom Line

Today’s competitive market makes it more important than ever to make a strong offer on a home. Reach out today 714.343.9294 to make sure you rise to the top along the way.

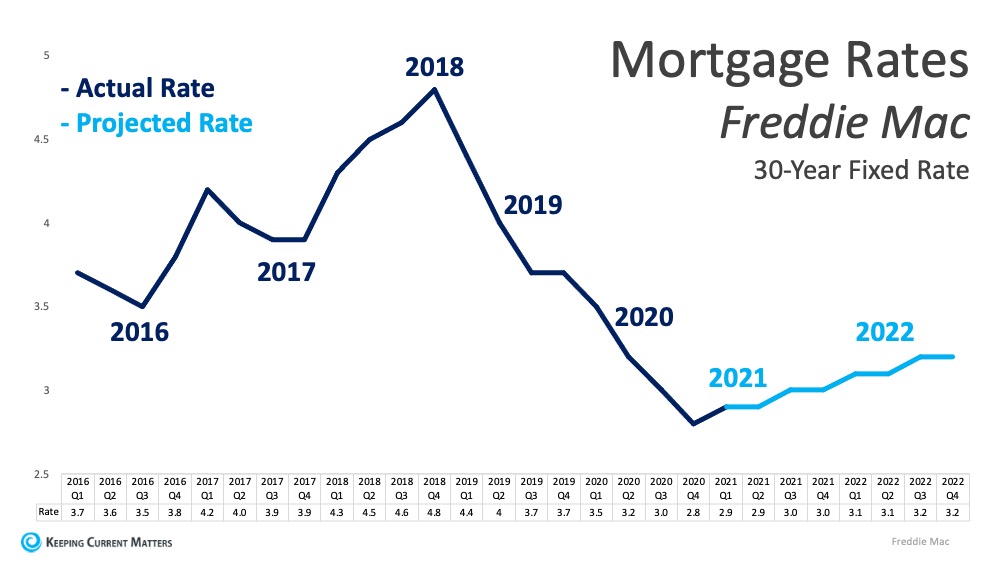

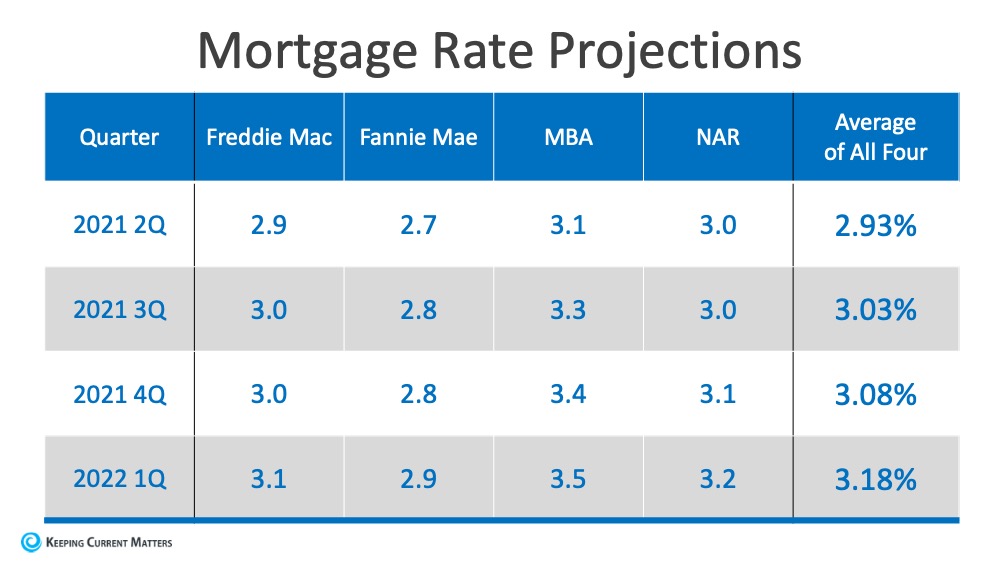

Freddie Mac isn’t the only authority forecasting low rates with a slight rise.

Freddie Mac isn’t the only authority forecasting low rates with a slight rise.

To Renovate or Not To Renovate Before You Sell

When thinking about selling, homeowners often feel they need to get their house ready with some remodeling to make it more appealing to buyers. However, with so many buyers competing for available homes right now, renovations may not be as vital as they would be in a more normal market. Here are two things to keep in mind if you’re thinking of selling this season.

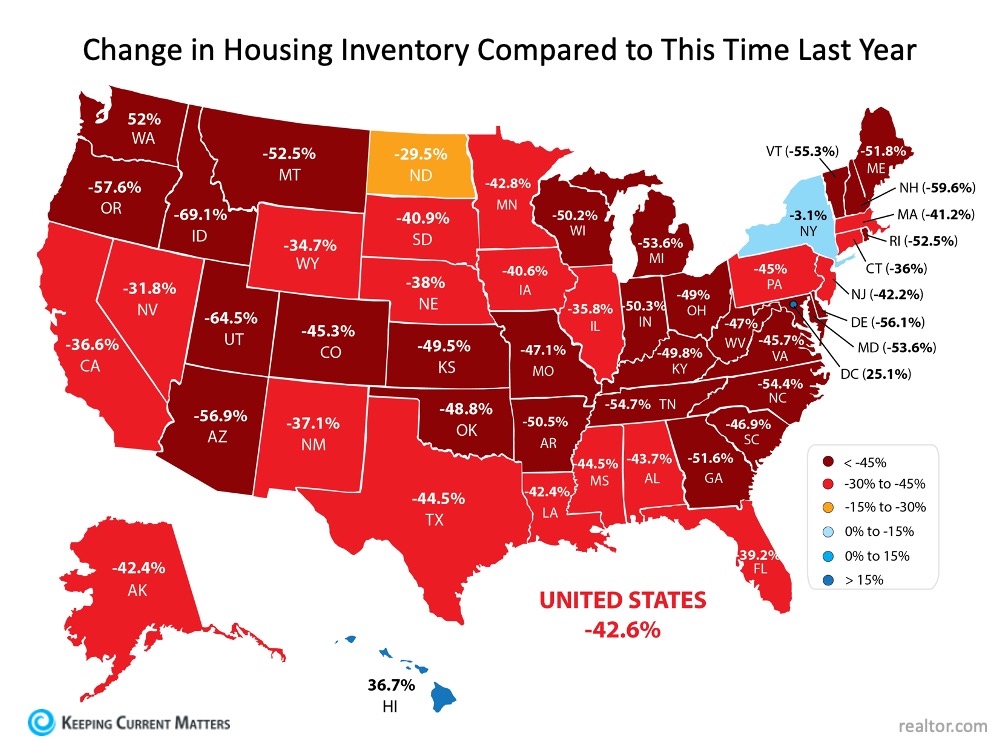

1. There aren’t enough homes for sale right now.

A normal market has a 6-month supply of houses for sale, but today’s housing inventory sits far below that benchmark. According to the National Association of Realtors (NAR), there’s only a 1.9-month supply of homes available today. As a result, buyer competition is high and homes are only on the market for about 21 days, during which time many receive multiple offers from hopeful buyers.

In a competitive market that’s moving so quickly, it makes sense to sell your house when buyers are scooping homes up as fast as they’re being listed. Spending costly time and money on renovations before you sell might just mean you’ll miss your key window of opportunity. While certain repairs on your house may be important, your best move right now is to work with a real estate advisor to determine which improvements are truly necessary, and which ones are not likely to be deal-breakers for buyers.

Today, many buyers are more willing to take on home improvement projects themselves in order to get the home they’re after, even if it means putting in a little extra work. Home Advisor explains:

In this market, it may be wise to let future homeowners remodel the bathroom or the kitchen to make design decisions that are best for their specific taste and lifestyle. As a seller, your dollars and time might be better spent working on small cosmetic updates, like refreshing some paint and power washing the exterior. Instead of over-investing in your home with upgrades that the buyers may change anyway, work with Stovall Team to determine the key projects that will maximize your listing, without overdoing it.

2. Focus on getting a good return on your investment.

When planning any bigger projects to tackle, you and Stovall Team will want to discuss the potential return on your investment and if those projects are worth the cost. Some homes do need a kitchen or bathroom renovation, roof repairs, or other major work, but definitely not all of them. You might be surprised by how well your house could fair in today’s sellers’ market. Hanley Wood states:

Ideally, homeowners getting ready to move should try to avoid over-investing in big renovations if they won’t make that money back when they sell their house. According to the 2020 State of Home Spending report from Home Advisor:

Before you renovate, contact Stovall Team at 714.343.9294 to see if it’s the best course of action. You may find out that putting your house on the market as-is will help you sell quickly, and it may result in the best return on your investment. Every home is different, but a conversation with your agent is mission-critical to make sure you make the right moves when selling this season.

Bottom Line

We’re in a strong sellers’ market, and that means you have the leverage to sell your house on your terms. Talk with Stovall Team today to determine if renovating is really the best way to spend your time and money before you sell.