-

Follow Us

-

Serving Fountain Valley and Orange County communities for over 35 years. (714) 343-9294 MICAH STOVALL #DRE01240489 Real Estate

Real Estate Just Listed Today in Fountain Valley CA

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Fountain Valley CA Real Estate with the Largest Lots

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Largest Price Reduced Real Estate in Fountain Valley CA

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Most Expensive Real Estate in Fountain Valley CA

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Most Square Footage in Fountain Valley CA Real Estate

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Least Expensive Real Estate in Fountain Valley CA

-

$659,990

17168 Newhope #222

Fountain Valley, CA -

$799,000

17793 Liberty

Fountain Valley, CA -

$879,000

17200 NEWHOPE St #31

Fountain Valley, CA -

$2,080,000

8715 El Lago Cir

Fountain Valley, CA -

$1,510,000

18430 Colville St

Fountain Valley, CA -

$1,549,900

9808 Sturgeon Ave

Fountain Valley, CA -

$473,000

16440 Atherton #26

Fountain Valley, CA -

$1,780,000

10449 APACHE RIVER Avenue

Fountain Valley, CA -

$549,000

12061 Brighton Riv, Unit 47 Riv

Fountain Valley, CA -

$1,569,999

18864 Cordata St

Fountain Valley, CA

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990Lot SizeN/A

Home Size1,112 sqft

Beds2 Beds

Baths2 Baths

-

$799,000Lot Size3.80 ac

Home Size1,980 sqft

Beds3 Beds

Baths2 Baths

-

$879,000Lot SizeN/A

Home Size1,920 sqft

Beds3 Beds

Baths3 Baths

-

$2,080,000Lot Size7,201 sqft

Home Size3,255 sqft

Beds7 Beds

Baths5.5 Baths

-

$1,510,000Lot Size7,201 sqft

Home Size1,984 sqft

Beds4 Beds

Baths2.5 Baths

-

$1,549,900Lot Size7,506 sqft

Home Size1,690 sqft

Beds4 Beds

Baths2 Baths

-

$473,000Lot Size4.00 ac

Home Size702 sqft

Beds1 Bed

Baths1 Bath

-

$1,780,000Lot Size6,068 sqft

Home Size2,710 sqft

Beds5 Beds

Baths2.5 Baths

-

$549,000Lot SizeN/A

Home Size916 sqft

Beds2 Beds

Baths1 Bath

-

$1,569,999Lot Size5,798 sqft

Home Size2,580 sqft

Beds5 Beds

Baths2.5 Baths

-

$659,990

17168 Newhope #222

Powered by WordPress. Built on the Thematic Theme Framework. test

Forget the Price of the Home. The Cost is What Matters.

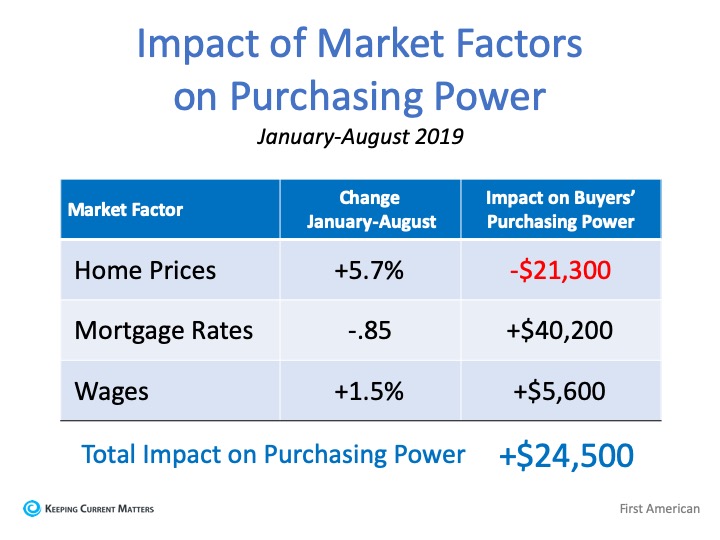

Home buying activing (demand) is up, and the number of available listings (supply) is down. When demand outpaces supply, prices appreciate. That’s why firms are beginning to increase their projections for home price appreciation going forward. As an example, CoreLogic increased their 12-month projection for home values from 4.5% to 5.6% over the last few months.

The reacceleration of home values will cause some to again voice concerns about affordability. Just last week, however, First American came out with a data analysis that explains how price is not the only market factor that impacts affordability. They studied prices, mortgage rates, and wages from January through August of this year. Here are their findings:

Home Prices

Mortgage Interest Rates

Wage Growth

When all three market factors are combined, purchasing power increased by $24,500, thus making home buying more affordable, not less affordable. Here is a table that simply shows the data:

Bottom Line

In the article, Mark Fleming, Chief Economist at First American, explained it best: